Dear friends and family,

The model portfolio's performance has been disappointing over the past 12 months as the market has rebounded from a historic bottom.

Why? In short, the model portfolio's stocks (the portfolio's engine) have failed to outperform the market. There are many plausible reasons for this related to the nature of this bounce back rally, but the reality is that our stocks have not recently produced excess returns. As a result, because the model portfolio's stocks are largely hedged against the general market, the model portfolio has not only underperformed the market but has actually produced a moderate loss (-15% since the model portfolio's all-time high point) in the past 12 months. This is a huge disappointment to me and is surely distressing to anybody that invested in the model portfolio's holdings near the market bottom of March 2009, after being buffeted by the market's huge losses of 2008-09.

To gain perspective on the model portfolio's performance, it is helpful to look at the model's performance over the full market cycle (since the market peaked in 2007) and also since the model's inception in 2003. The two charts posted here will hopefully provide some useful insight, especially if you share my long-term orientation.

As the charts show, the model has proved to produce huge gains when in-phase with the market conditions, such as the period from May 2003 to March 2009 when it piled up a cumulative gain of 768%. And over the past year while the model has been out-of-phase with the market conditions, it has produced a loss of approximately -15%. That is a very attractive risk-return in my book.

Because it is clear the model is currently out-of-phase with the market conditions and is getting near its designed maximum loss limit of -20%, I am reducing the position size in my personal portfolios and those that I manage for friends and family. Once I see that the model portfolio is again pumping out profits over a 13-week (3 month) and 26-week (6 month) timeframe I will return to a normal position size in my portfolios.

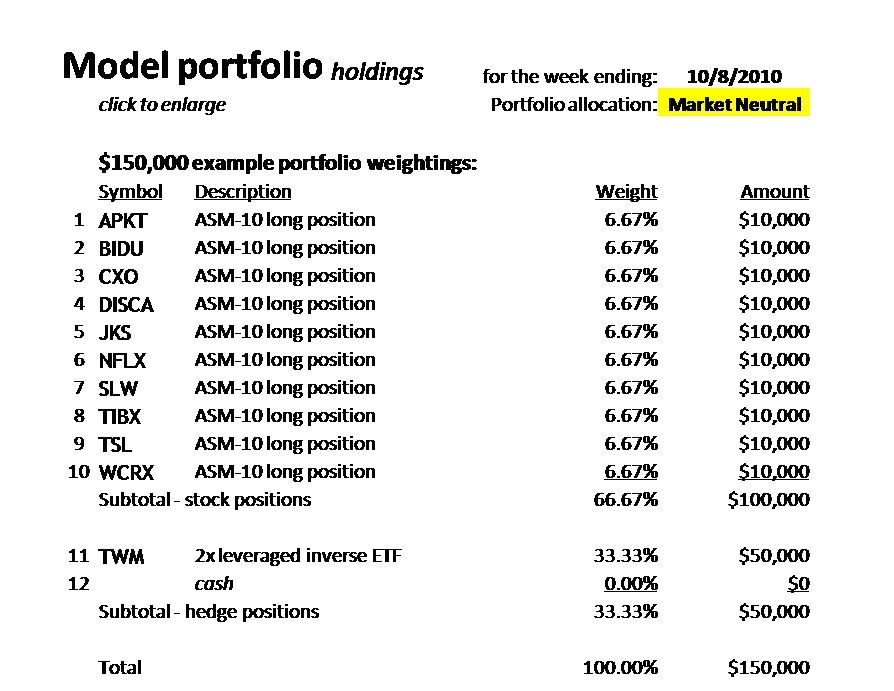

What does this mean? As an example, instead of investing $10,000 per holding as per the model portfolio shown here, I will now invest $5,000 per holding, and thereby hold more cash. This will dampen our risk, but at some cost because it will also reduce the opportunity for gain in the first weeks of an upturn in the model's performance. This is a good time to be prudent and there is no need to swing for the fences since clearly the model is not currently behaving as expected. By keeping the majority of our capital intact, we will be in position to take advantage of the next opportunity for outsized gains.

Note that the weekly results shown on this blog will continue to be based on a full position size for each holding. Also note that your actual performance my vary somewhat from the model portfolio's due to tracking error... e.g. since our actual trades are executed on Monday whereas the model portfolio's returns are based on Friday's closing prices. Rest assured that I also see tracking error in my personal portfolios because my trades are also placed on Monday, same as yours.

Please feel free to send me an email with any questions or comments and I will do my best to respond. Due to my desire to protect the anonymity of everybody here, I won't be responding to any comments posted on this blog.